The Overlooked Middle: Opportunities in $5-50M Exits for Tech Companies

The new playbook of building asset-light, AI-native tech businesses designed for multiple exit pathways

TLDR:

Market Opportunity: The $5-50M exit range represents a significant arbitrage opportunity systematically ignored by traditional VC. While VCs chase unicorns, over 75% of tech exits occur in this "overlooked middle."

AI-Powered Economics: AI has dramatically reduced the cost and timeline of building software companies, making previously overlooked markets ($10-100M TAM) highly attractive.

Multiple Exit Pathways: Companies in this range benefit from diverse acquirers (micro-PE, search funds, strategics) with 2-4 year timelines versus VC's 7-10 year unicorn pursuit.

Superior Returns: This approach delivers better risk-adjusted returns through higher success rates (>40% vs <5%), faster liquidity, and QSBS tax advantages enabling up to $10M in tax-free gains.

Antifragile Design: Our thesis-driven studio creates resilience through balanced portfolio construction spanning stable cash-flow businesses, middle-market exits, and venture-scale potential

An Overlooked Market

VCs systematically ignore companies with $5-50 million exit potential—not by accident, but by mathematical necessity.

Their economics are doubly constrained: they invest at sky-high valuations in competitive markets where power law returns demand unicorn outcomes, and their 2/20 fee structure incentivizes raising massive funds ($1B funds generate $200M in management fees regardless of performance) that require large check sizes. This model inherently sidelines companies aiming for more modest, yet substantial exits to PE funds or strategics.

As AI dramatically reduces development costs and timelines, companies targeting modest markets can now achieve profitability faster and with less capital. This overlooked middle market represents a perfect arbitrage opportunity. By building asset-light, AI-native businesses designed for multiple exit pathways, it is feasible to achieve exits in 2-4 years instead of 7-10, with significantly higher success rates and without sacrificing potential returns.

The state of Venture Capital

As described in our previous article, the venture capital model is experiencing unprecedented pressure from multiple directions.

With over $1.5 trillion in dry powder across private markets and a 75% decline in IPO volume compared to historical averages, the traditional exit pathways are constricting while competition for deals intensifies.

Data from Cambridge Associates shows that venture capital returns have been declining for decades. The median VC fund barely returns capital after fees, while top-quartile performance has dropped from 30%+ IRRs in the 1990s to mid-teens today. Meanwhile, check sizes have grown 3x in the last decade while time-to-exit has extended to 8-10 years on average.

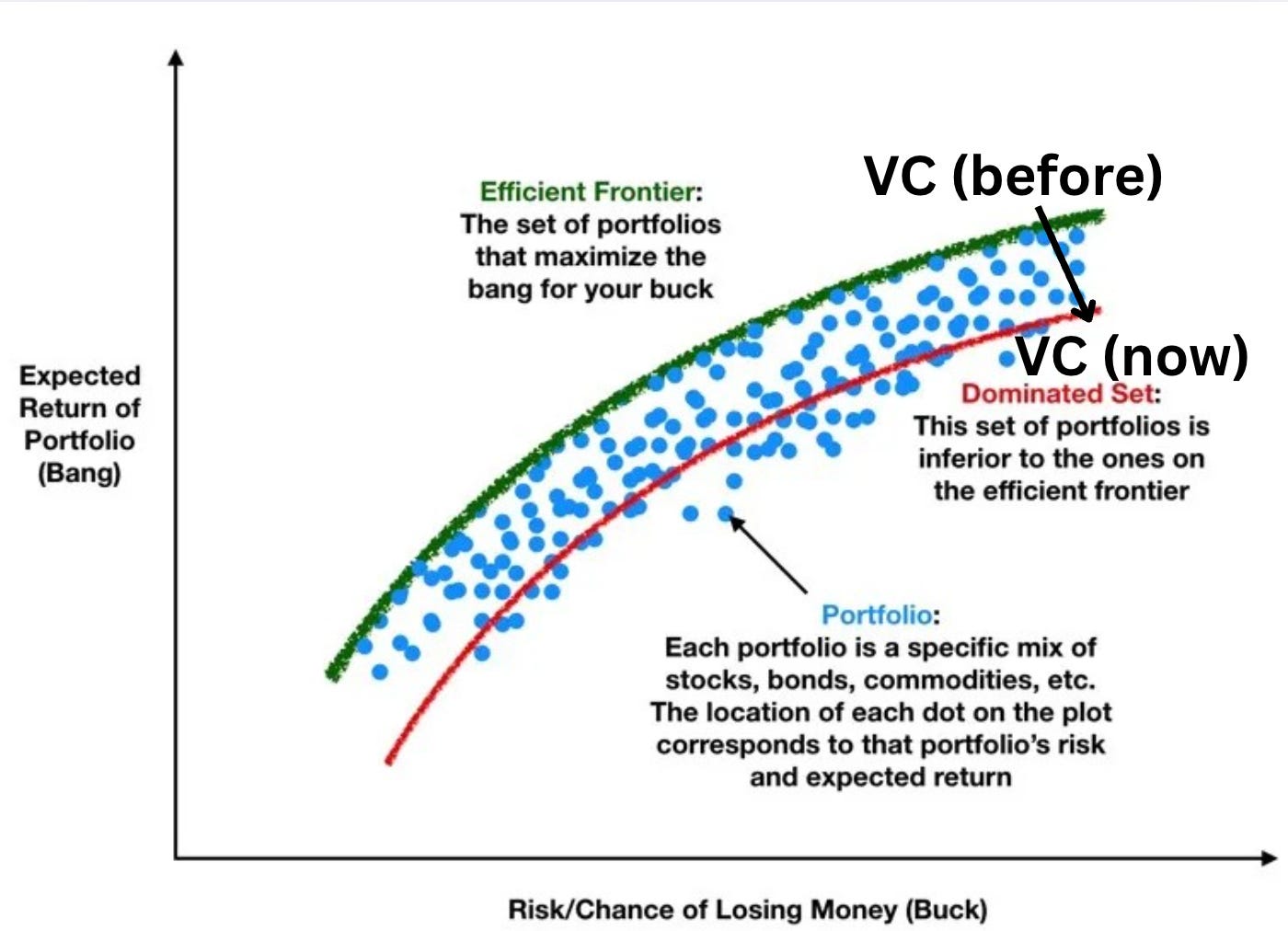

These trends have pushed traditional VC below the efficient frontier, creating a mathematical mismatch between risk and reward. The model is failing both founders (who face extreme dilution and binary outcomes) and limited partners (who endure extended illiquidity for diminishing returns).

The Robust Middle Market PE/Strategic Landscape

Despite challenges in the broader PE market, such as longer holding periods and reduced liquidity, the lower middle market ($5-100M in annual revenue) remains robust, with approximately 350,000 U.S. companies in this segment.

According to Bain & Company’s 2024 Global Private Equity Report, 67% of PE firms have increased their focus on acquisitions under $50M in enterprise value, citing lower competition and attractive valuation multiples. In 2023, the median PE buyout multiple for such companies was 7.4x EBITDA, with firms generating $1-5M in EBITDA attracting an average of 12 potential buyers.

This landscape has been energized by the rise of micro-PE firms, independent sponsors, and search funds targeting tech acquisitions in the $5-50M range:

Micro-PE Funds: Managing pools typically under $100M, micro-PE firms focus on SaaS, e-commerce, and IT services companies with $1-5M in EBITDA. Their growth, fueled by online deal-sourcing platforms and flexible family office funding, has expanded the buyer pool, increasing competition for middle-market tech firms.

Independent Sponsors and Search Funds: Independent sponsors raise capital per deal, while search funds involve individuals acquiring and operating a single business valued between $5M and $30M. The Stanford Search Fund Study reports record growth in search funds, with many targeting tech and software companies, diversifying the buyer landscape.

Impact on Deal Dynamics: These emerging players have made the $5-50M market more competitive, often benefiting sellers. A software company with $3M in EBITDA might attract bids from traditional PE funds, micro-PE firms, search funds, and strategic acquirers, driving up valuations. In tougher markets, such as 2022-2023, these smaller buyers remained active, using creative financing to sustain deal flow.

The Thesis-Driven Studio Model

To capitalize on the middle market opportunity, a thesis-driven studio model is optimal. This approach involves experienced operators with domain expertise, proprietary data access, and established distribution channels collaborating to build profitable, AI-native businesses designed for multiple exit pathways.

This model creates antifragility by design across the risk-return spectrum through three distinct company categories:

1. Cash-Flow Generating Companies (1-2x) - Downside Protection

The studio model excels at downside protection by converting what traditional VCs would consider "failures" into steady cash-generating assets. By focusing on profitability from day one, companies that don't achieve rapid growth aren't abandoned but instead streamlined into efficient businesses that return capital while requiring minimal oversight. This approach maximizes chances that even the "failures" in the portfolio become productive assets rather than write-offs.

2. Companies Targeting PE/Strategic Exits - The Core Focus

The heart of the thesis-driven studio model targets this middle category – B2B companies built specifically for acquisition by private equity firms or strategic buyers at valuations between $10-50M. These companies leverage AI to achieve profitability faster with less capital, making them ideal acquisition targets.

By focusing on this overlooked middle market, the studio model creates businesses with multiple potential exit pathways rather than the binary outcomes of traditional VC. This category offers the optimal balance between risk and return, with significantly higher probability of success than venture-scale outcomes and substantially higher returns than pure cash-flow businesses.

3. Venture-Scale Successes (10-100x) - Asymmetric Upside

While not the primary target, the studio model maintains exposure to exceptional outcomes. Through strategic portfolio construction, even a small percentage of venture-scale successes can generate outsized returns that cover dozens of smaller outcomes. As shown in the spectrum, while the probability of these extreme outcomes is smaller (narrower green area), their magnitude is sufficient to drive fund-level returns.

Unlike traditional VC that relies exclusively on these rare outcomes, the studio model views them as complementary to the more predictable exits. This creates true asymmetric upside – exceptional returns remain possible without requiring the fund economics to depend on them.

By designing companies with multiple potential outcomes from inception, the thesis-driven studio creates convexity in its portfolio—the probability of success grows faster than the associated risks. This fundamental shift in approach allows for venture-scale returns with dramatically reduced downside, creating a truly antifragile investment strategy.

Examples of the Thesis-Driven Studio Approach:

Healthcare Operations Studio: Collaborating with former hospital administrators to build AI-powered operational efficiency tools for specific healthcare workflows (patient intake, billing optimization, or inventory management) and targeting a $30M exit to healthcare services roll-ups within 3 years.

Financial Advisory AI: Working with a network of financial advisors to develop specialized AI tools that automate routine portfolio management while maintaining the full client relationship and revenue stream, rather than just selling software to advisory firms.

SMB Services Modernization: Building AI-powered back-office solutions for specific SMB segments (restaurants, dental practices, HVAC contractors) by partnering with industry veterans who have distribution channels into these fragmented markets.

Expanded Exit Pathways Beyond PE

Strategic Acquisitions Driven by AI Disruption

Many legacy SaaS companies will need to acquire AI-native startups or be displaced, creating an M&A exit boom. According to PitchBook data, acquisitions of AI companies under $50M have increased by 43% year-over-year, with legacy software companies now accounting for 39% of all such acquisitions.

This trend is accelerating as large public SaaS companies recognize the existential threat from AI-native competitors. Companies like Salesforce, Adobe, and ServiceNow have collectively set aside over $10 billion for AI acquisitions, with a significant focus on companies in the $15-40M valuation range.

AI-Driven Roll-Ups & Industry Arbitrage

The Efficiency Arbitrage

AI unlocks cost reductions that legacy businesses can't match. For example, an SMB accounting firm could see margins jump from 30% to 60% using AI. This allows AI-native firms to outcompete incumbents or roll them up profitably.

Control vs. SaaS Selling

Buying legacy businesses and layering AI is smarter than competing with VC-funded software startups. Owning a profitable business that generates proprietary data gives you an advantage over a SaaS startup trying to sell into a reluctant industry.

The data supports this approach: McKinsey's Digital Transformation Survey found that 62% of businesses cite implementation challenges as the primary reason for delaying AI adoption. By acquiring these businesses rather than selling to them, founders can bypass adoption resistance entirely.

Data Farms: The New M&A Thesis

Middle-market companies will increasingly be acquired not for their operations, but as "data farms" to train specialized AI models, creating a new M&A thesis centered on proprietary data accumulation rather than traditional financial metrics. Companies in sectors like healthcare, legal services, or SMB operations generate vast amounts of niche, proprietary data (e.g., patient records, legal documents, or transaction histories) that are highly valuable for training AI models.

This could lead to a new type of roll-up where the goal is to aggregate datasets across a sector, creating a dominant AI model that can be licensed or sold. As the "oil" of the AI economy, proprietary data with high signal-to-noise ratios will command significant premiums, making otherwise unremarkable middle-market companies suddenly valuable acquisition targets.

Venture-Scale Value Capture Without Venture Risk

The Full Revenue Stack

Traditional vertical SaaS models don't capture enough industry value. A software company selling to accounting firms might get a 3-4% take rate, whereas an AI-powered accounting firm owns the entire revenue stream.

The economics are striking: A SaaS platform serving the legal industry typically captures $100-250 per user per month, representing 3-5% of industry revenue. By comparison, an AI-enabled legal service provider captures the entire client fee—a 20-33x difference in revenue potential.

Data Defensibility

Owning the service layer allows for AI defensibility. By operating the business directly, you control proprietary data and build AI models that competitors can't access.

This creates a virtuous cycle: proprietary data improves AI capabilities, which enhances service delivery, which generates more proprietary data. According to MIT research, AI models trained on proprietary vertical data outperform general models by 40-70% on domain-specific tasks.

Tax Advantages and Faster LP Returns

There's an additional tax advantage for both founders and investors: companies exiting at sub-$50 million valuations can potentially qualify for QSBS (Qualified Small Business Stock) treatment, allowing for tax-free gains on a significant portion of returns—an advantage lost when companies raise at higher valuations.

For limited partners, this approach delivers a critical benefit: faster return of capital. While traditional venture funds might not return significant capital until years 7-10, companies built for PE acquisition can generate liquidity events in years 2-4, dramatically improving fund IRRs and allowing for capital recycling. Recent Cambridge Associates data shows that funds specializing in companies with exits below $50M return capital 2.7x faster than traditional early-stage venture funds.

Comparative Returns Table

A Systematic Approach

The structural misalignment between how most venture capital is deployed and how value is increasingly created has opened space for new models of company formation. As AI accelerates development timelines and compresses product cycles, opportunities for faster, smaller, and more frequent exits have expanded—particularly in the $5–50M range, which traditional VC models are structurally disincentivized to pursue.

ZeroVC’s studio framework is designed to address this gap by building businesses that span a broader range of risk-return outcomes. Our model, inspired by Howard Marks’ risk-return matrix, avoids clustering risk at one extreme and instead constructs a portfolio with a blend of:

Cash-flow-generating businesses that provide stability and capital return

Companies built for targeted $5–50M exits (e.g., strategic M&A, PE, industry rollups)

Outliers with venture-scale upside

This approach is designed to improve capital efficiency, enable faster liquidity for LPs, and reduce dependence on rare, high-variance outcomes.

For Investors: The model provides superior risk-adjusted returns by systematically exploiting the structural inefficiencies in venture capital and leveraging the transformative efficiency of AI-native company building.

For Operators: This approach creates a framework for building valuable companies without the binary pressure of unicorn-or-bust outcomes, enabling more sustainable growth and multiple pathways to success.

For Corporates: The studio model presents opportunities to partner early with AI-native companies addressing industry-specific challenges, with potential for strategic acquisition or data collaboration.